Executive summary

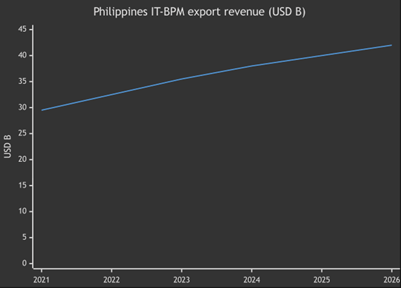

The Philippines IT BPM industry is heading into 2026 with a clear shift. More of the growth is coming from higher value work, even though big contact center programs still drive the bulk of the volume. Export revenue was reported at $29.5B in 2021, then $32.5B in 2022, $35.5B in 2023, and $38.0B in 2024. The sector is tracking around $40B in 2025 and about $42B in 2026E. [1]

Three growth engines stand out as “where the growth is really coming from:”

1) GCCs and GICs are lifting the value mix. In 2024, they were reported at about 250k employees and around $8B in revenue, roughly 20 percent of the total. Industry leaders have also been clear that GCC growth is outpacing the broader market (starting from a smaller base) and that it needs policies designed specifically for GCC expansion. [2]

2) Vertical specialization in BFSI and healthcare continues to outperform. Specialization by industry is still paying off, especially in BFSI and healthcare. BFSI is called out as the largest vertical served from the Philippines, at over 25 percent share. Healthcare is often placed at around 11 to 15 percent and keeps getting mentioned as a key contributor to growth. [3]

3) Digital/IT services demand is rising, but the constraint is talent, not demand. The guidance keeps pointing to upskilling for AI, cybersecurity, IT support, and analytics. This lines up with global spending momentum in AI and IT, which helps fund cloud moves, security programs, and automation-driven operations. [4]

Over a 3–5 year horizon (2026–2030), a scenario-based outlook is most defensible because the official roadmap targets are ambitious and are being reviewed midstream. Under a steady-growth base case (~7% CAGR), export revenue would reach ~$55B by 2030; under a constrained (~5%) scenario, it reaches ~$51B, and under an upside (~9%) scenario, it reaches ~$59B. These trajectories are anchored to the industry’s 2026 export guidance and global demand tailwinds (IT spending and AI spending growth), while recognizing execution and constraint risks (talent, power, infrastructure, policy clarity). [5]

Actionable implications:

- Investors: The most scalable opportunities are in three areas. First, GCC platforms and campus-style ecosystems where global companies set up their own delivery centers. Second, specialized service providers focused on BFSI and healthcare, since those sectors keep expanding faster than others. Third, digital infrastructure such as data centers, fiber networks, and telecom towers. These investments reduce operational risk and allow outsourcing work to expand into more locations across the country. [6]

- Service providers: The real margin growth is unlikely to come from basic voice support alone. It is more likely to come from bundled transformation deals that combine customer experience, back office operations, data and AI work, and cybersecurity services in one contract. Another key shift is moving talent into digital and data-related services rather than relying only on transactional contact center work. [7]

- Policymakers: Competitiveness will largely depend on three things. First is improving the quality of the talent pipeline through education and upskilling. Second is creating predictable incentives and aligning national policies with local government units. Third is strengthening the power and connectivity infrastructure. These factors are critical because they directly affect the ability to attract GCC investments and expand outsourcing operations outside major metro areas. [8]

Market size and growth outlook

Recent performance and the current baseline are fairly easy to see when you look at the last few years of industry data. The Philippines’ IT BPM sector has continued to grow steadily, both in export revenue and in employment. The numbers below summarize the trajectory reported by industry groups and the major business press. The 2026 figure is a forward estimate. [1]

| Year | Export revenue (USD B) | YoY growth | Direct employment (M FTE) | YoY growth | Notes |

| 2021 | 29.5 | — | ~1.42 | — | Post‑pandemic rebound year cited in industry reporting [1] |

| 2022 | 32.5 | ~10.2% | 1.57 | ~10.6% | BFSI and healthcare cited as key growth contributors [1] |

| 2023 | 35.5 | ~9.2% | 1.70 | ~8.3% | 2023 revenue and jobs reported at campaign launch [7] |

| 2024 | 38.0 | ~7.0% | 1.82 | ~7.1% | 2024 record-high jobs and revenue widely reported [4] |

| 2025 | ~40.0 | ~5.3% | ~1.90 | ~4.4% | 2025 growth/recalibrated targets communicated mid‑2025 [2] |

| 2026E | 42.0 | ~5.0% | 1.97 | ~3.7% | 2026 export revenue and headcount guidance [5] |

Role in the global services landscape. The Philippines is widely recognized as the number two global IT BPM delivery hub after India. [14], with a ~16–18% share of global offshore/nearshore IT‑BPM headcount in one industry roadmap framing. [15]

That position reflects a long-standing role in global services. The Philippines has become a major center for contact center operations, back office processing, finance and accounting support, healthcare administration, and a growing share of IT and digital services. For many multinational companies, it remains one of the core locations used to run large-scale service delivery.

Near-term forecast. Global demand conditions matter a lot because the Philippines still serves mostly international clients. One industry roadmap snapshot shows the buyer mix at roughly 70 percent North America, about 15% Europe, including the United Kingdom, and another 15% from the Asia Pacific region. [16] In 2026, worldwide IT spending is expected to reach about $6.15 trillion in 2026, which represents growth of around 10.8 %. Global AI spending is forecast to reach about $2.52 trillion, expanding by roughly 44 percent. Both trends support demand for managed services such as cloud operations, cybersecurity, data services, and automation-driven workflows that are commonly delivered through IT BPM models. [17] IMF’s January 2026 WEO Update projects global growth ~3.3% in 2026 (macro stability tailwind, though not a guarantee of outsourcing acceleration). [18]

Time-series chart (revenue). (Data points correspond to the table above.) [1]

Forecasts (2026–2030). Because the Roadmap 2028 targets are under midterm review and because 2025–2026 guidance implies moderate growth, the most rigorous presentation is a scenario band anchored to 2026 guidance rather than a single-point estimate. [19]

| Scenario (illustrative) | Assumption (2026–2030) | 2030 revenue (USD B) | What must go right |

| Constrained | ~5% CAGR | ~51 | AI substitution hits low-complexity work faster; talent constraint binds; power and connectivity remain high-friction [4] |

| Base case | ~7% CAGR | ~55 | GCC expansion continues; BFSI/healthcare stay strong; digital services scale with upskilling [2] |

| Upside | ~9% CAGR | ~59 | Step-change in value mix (GCC + digital/data and cyber) and faster productivity / revenue-per-FTE uplift [2] |

Revenue by service line

What can be measured cleanly vs. what must be estimated

Public reporting in the Philippines is strong on total export revenue, employment, and some mix indicators, but does not consistently publish detailed revenue breakdown across specific service lines such as cloud services, cybersecurity, AI and machine learning, analytics, or other digital capabilities. Therefore, this section explicitly separates:

- Reported anchors (industry roadmap mix and segment sizing); and

- Analytical allocations (internally consistent with the anchors; presented as ranges, not false precision).

Reported anchors for service-line economics

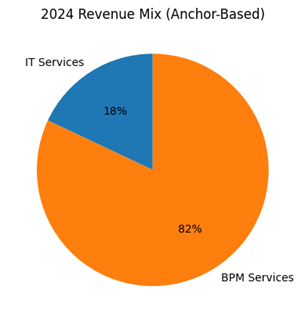

A key industry roadmap snapshot (2022E) describes the market at roughly $31B to $33B in revenue and about 1.5M to 1.6M workers. In that mix, IT services contributed around 16 to 18 percent of total revenue, while BPM services represented about 82 to 84 percent. [23] Using those shares, IT services revenue would have been roughly in the $5B to $6B range at that time. BPM services would have been around $26B to $27B. These numbers line up directionally with the overall revenue totals reported for the industry. [24]

The same roadmap highlights that “digital and data services” (explicitly including AI/ML, cloud/mobile app development, IoT, big data, D&A, cybersecurity within infrastructure services) is a priority expansion lane for the Philippines. [25]

2024 estimated revenue by service line

Using 2024 export revenue of $38B as the scaling base, and applying the 2022E mix shares as an anchor (while recognizing possible drift), the following range-based decomposition is analytically consistent with published revenue totals and mix statements. [26]

| Service line (requested taxonomy) | 2024E revenue range (USD B) | Share (illustrative) | Evidence anchor |

| BPO voice (contact center voice + voice-heavy CX) | ~13–17 | ~35–45% | Contact center/CX is repeatedly described as a core maturity area; volume remains strong [3] |

| BPO non-voice / back office (F&A, HR, procurement, ops support) | ~11–15 | ~30–40% | BPM is ~82–84% of revenue (2022E); non-voice BP and functional services are emphasized as mature deliveries [3] |

| KPO / judgment-intensive BPM (e.g., industry research, advanced F&A/FP&A, trust & safety) | ~2.5–5.0 | ~7–13% | Roadmap highlights judgment-intensive BPM, Trust & Safety, and data/analytics-enabled BPM as growth lanes [3] |

| Software development/app services (ADM, product engineering components) | ~2.0–3.5 | ~5–9% | IT services are ~16–18% of revenue and shifting toward more complex services [3] |

| Cloud services (cloud ops + cloud migration) | ~1.0–2.0 | ~3–5% | Explicitly cited within IT infra + next-gen delivery emphasis [3] |

| Cybersecurity services | ~0.6–1.5 | ~2–4% | Explicitly cited as an in-demand upskilling target and part of IT infra services [6] |

| Digital transformation (process + tech transformation programs) | ~1.0–2.5 | ~3–7% | Roadmap emphasizes end-to-end transformation and bundled deals across functions [6] |

| AI/ML + intelligent automation (build/ops/enablement) | ~0.4–1.2 | ~1–3% | AI is framed as augmenting work; upskilling priority; global AI spend growth supports demand [4] |

| Analytics/data services (BI, D&A, data engineering) | ~0.8–2.0 | ~2–5% | Roadmap repeatedly calls out D&A as a major growth segment [3] |

| R&D / engineering services | ~0.2–0.8 | ~0.5–2% | Supported directionally by upmarket “product/services complexity” push; less directly quantified [3] |

The Philippines’ near-term revenue is still dominated by BPM (voice and non-voice), but the incremental growth (and margin resilience) is increasingly tied to GCC scaling and digital/IT capabilities where buyers pay higher effective revenue per employee. [37]

Revenue mix chart (high-level)

(Shown at the BPM vs. IT services level because that is directly supported by published mix statements.) [38]

Revenue by end‑market sector and where demand is concentrated

A roadmap snapshot provides an indicative industry-vertical distribution served from the Philippines: BFSI >25%, Tech/Media/Telecom ~14–18%, Retail ~14–18%, Healthcare ~11–15%, Manufacturing <6%, Energy <6%, Others >25%. [16] With 2024 revenue at $38B, this implies the following ranges.

| End-market sector (requested) | Proxy category in roadmap | 2024 revenue range (USD B) | What’s inside this bucket |

| Finance | BFSI | >9.5 | Banking ops, cards, fraud, KYC/AML support, claims, analytics, customer ops [3] |

| Healthcare | Healthcare | ~4.2–5.7 | Payer/provider ops, coding/billing, clinical support and analytics growth lanes [3] |

| Telecom | Part of TMT | ~5.3–6.8 | Customer ops + digital ops; overlaps with big tech/platform work [3] |

| Retail/e-commerce | Retail | ~5.3–6.8 | Customer ops, trust & safety, digital CX, fulfillment-related support [3] |

| Manufacturing | Manufacturing | <2.3 | Industry ops, supply chain support, shared services [3] |

| Public sector | Mostly “Others” | part of >9.5 | Government digital services support and other public-adjacent work (not separately sized here) [3] |

| Gaming | Part of “Others” and creative services | small but fast-growing | Game dev/animation services are tiny but high-growth niches in the roadmap [3] |

Buyer geography remains highly concentrated: ~70% North America, ~15% Europe, ~15% APAC in one roadmap snapshot. [16] This concentration matters for outlook because US demand cycles, regulation, and AI adoption patterns largely set the pace for Philippine delivery volumes and pricing. [42]

Geographic hubs and the role of regional centers

The Philippines’ growth story in IT‑BPM is increasingly a “multi-hub” story rather than a single-metro story.

- The industry previously reported ~31% of headcount in the countryside (outside Metro Manila) by end‑2022, and more recently described being at ~32% outside Metro Manila (from ~25% pre‑COVID), with a roadmap ambition to reach ~40% by 2028. [43]

- Industry reporting points to expansion in Cebu, Davao, Bacolod, Pampanga, and Laguna as examples of non‑Metro Manila growth nodes. [43]

Hub comparison table

| Hub | Typical role(s) in the delivery system | Why it matters for growth economics |

| Metro Manila | Primary location for headquarters, complex multi-tower delivery, many GCCs; deepest management bench | Highest revenue density; greatest congestion risk; policy clarity and infrastructure reliability have outsized impact [2] |

| Cebu City | Mature secondary hub spanning CX + shared services; also hosts some GCC footprint (often paired with Metro Manila) | Diversifies delivery concentration; supports scale with lower friction and a strong talent pool [2] |

| Davao City | Key Mindanao hub for CX and back office; resiliency through geographic diversity | Expands recruitable labor pool; supports multi-site continuity planning [1] |

| Bacolod City | Recognized provincial delivery node; often used for scalable CX and selected back office | Cost and retention advantages: helps decongest Metro Manila [1] |

| Iloilo City | Emerging/maturing Visayas hub; services expansion outside top two metros | Broadens the national footprint; increases labor participation from new catchments [10] |

| Clark Freeport Zone | Hybrid metro-industrial hub; proximity to Metro Manila with different congestion profile | Attractive for risk diversification and new campus builds, especially as digital infra expands [10] |

Role of regional centers in the next growth phase. The push toward regional delivery hubs is not just about lowering costs. It is also about reducing risk and widening access to talent. In large metro areas, daily commuting has become a major friction for workers. Long travel times affect productivity, retention, and overall workforce stability. Regional centers can ease this pressure by allowing companies to tap talent closer to where people actually live.

Global buyers increasingly want geographic diversification in their delivery networks. Spreading operations across multiple cities helps avoid over-concentration in a single location and improves operational resilience. Because of this, the expansion of IT BPM activity into regional areas is often framed as both a workforce solution and a requirement for global clients managing delivery risk. [2]

Demand drivers and supply-side constraints

Demand drivers that plausibly sustain growth through 2030

Global digitization and AI capex are reinforcing managed services demand. With worldwide IT spending expected to expand in 2026 and AI spending growing even faster, buyers have structural incentives to externalize parts of (a) modernization, (b) cyber operations, and (c) data/AI operations, especially where talent shortages constrain onshore execution. [54]

BFSI and healthcare remain “sticky” verticals. BFSI and healthcare are repeatedly identified as the Philippines’ growth drivers; these verticals also allocate significant budget to compliance operations, risk/fraud, claims/coding, and analytics-heavy functions, well-suited to GCC and higher-skill BPM models. [55]

GCC buildout is a structural shift, not a cyclical spike. Industry reporting highlights increased interest from investors in the US, Australia[56], and Europe for GCC setups, and explicitly characterizes GCCs as “strategic engines” rather than mere cost centers (mirroring India’s evolution). [57]

Supply-side factors and the binding constraints

Talent pipeline is large, but “job-ready digital talent” is the constraint. A roadmap skills snapshot cites ~850k annual graduates, ~4.4M enrollees, and ~2,418 HEIs, but also emphasizes the need for a continuous supply of quality, digital-ready talent. [58] The risk is “not being skilled enough,” with repeated calls for upskilling/reskilling in AI, cloud, cybersecurity, and analytics. [59]

Connectivity and last-mile reliability become more important as hybrid work and regionalization expand. The Department of Information and Communications Technology[60] has positioned digital connectivity as a national priority through an approved National Digital Connectivity Plan, including ambitious broadband speed targets. [61] Separately, government reporting cites the operational rollout of a national fiber backbone phase connecting provinces, eco-zones, and government data centers, relevant because it expands the feasible hub set for IT‑BPM delivery beyond top metros. [62]

Data centers and cloud infrastructure are becoming a competitiveness lever. A major constraint for higher-value digital work is local compute and resilient connectivity. Reported developments include joint ventures and scale-up plans among major operators, as well as new data center projects and expansions aimed at cloud and AI workloads. [63]

Power cost is a real limit for 24/7 operations and data centers. A WTO case study notes that the Philippines has among the highest industrial electricity rates in Southeast Asia (citing DOE 2025), directly affecting energy-intensive sectors like data centers and 24/7 BPO delivery. [64] Market data also shows the Philippines’ power prices remain elevated relative to many peers, even with potential downward pressure from renewables over time. [65]

Investment, M&A activity, policy, and incentives

Policy and incentives shaping the operating model

The post‑pandemic policy arc matters because delivery flexibility (WFH/hybrid) directly affects (a) labor supply, (b) retention, and (c) the viability of regional scaling.

- In 2022, Department of Finance[66] clarified that IT‑BPM firms could adopt WFH, but firms that wanted to keep ecozone incentives still had to follow the rule that work must be done within zone boundaries. That created a real trade-off between flexibility and incentives.[67]

- The CREATE MORE Act (RA 12066) and its rollout were presented as a way to make incentives more competitive and easier to plan around. It includes provisions that allow telecommuting and work from home up to a certain threshold and clarifies VAT and incentive mechanics, which matters a lot for export-oriented services firms. [68]

- A common working interpretation is up to 50 percent hybrid for some registered firms. Industry interpretation of the implementing framework is that registered IT BPM enterprises under investment promotion agencies can allow up to 50 percent hybrid work, with the exact details depending on how the firm is registered and what rules apply to its incentive setup. [69]

Policy execution risk remains at the local level. Even when national policy is clear on paper, implementation can get messy at the local level. Industry reporting points to issues with how local government units interpret and apply the rules, with plans to issue clearer joint guidance. [12]

Investment and M&A signals relevant to IT‑BPM growth

Even though IT BPM is technically a services industry, its future growth is increasingly tied to investments in digital infrastructure. The ability to run cloud operations, AI workloads, and distributed service teams depends heavily on the strength of the country’s connectivity and compute capacity.

Several recent investment signals highlight how infrastructure and services are becoming closely linked.

- PLDT[70] has been reported to be in talks to sell up to 49% of its data center business to NTT[71], a signal that investors are valuing Philippine data center capacity as a strategic asset tied to AI/cloud demand. [72]

- KKR[73] announced a $400M investment in telecom towers expansion/operations in the Philippines. Tower infrastructure may sound like a telecom story, but it directly supports distributed service delivery by improving connectivity and network reliability across more regions. [74]

- Alibaba Cloud[75] announced plans to launch a second data center in the Philippines (reported timeline: by October 2025), reinforcing the country’s growing relevance as a cloud node in Southeast Asia. [76]

- Data center operators have also organized industry coordination efforts, reflecting both growth expectations and the need to align on standards/policy for expansion. [77]

On the services side, the most important long-term investment theme is the continued buildout of Global Capability Centers. Industry reporting notes that the Philippines aims to become a larger GCC hub and that these centers require different incentive structures compared with traditional BPM providers. This suggests that policy frameworks may evolve further to support a new wave of GCC-related investment. [57]

Risks, constraints, and quantified opportunity sizing

Key risks to the 2026–2030 outlook

Competition and buyer diversification. The Philippines operates in a market where India holds the dominant offshore share, and multiple nearshore/offshore markets (Europe nearshore, Latin America, and “rest of APAC”) compete for incremental work, especially as buyers diversify concentration risk. [78]

Automation and AI-driven substitution risk is real but uneven. Industry survey evidence reported in 2024 indicates mixed impacts: some firms report headcount reductions due to AI while others report headcount gains, consistent with the view that AI shifts task composition before it reduces total employment. [79]

Data governance and privacy compliance are non-negotiable for upmarket work. As the Philippines moves further into regulated sectors and digital services, data protection frameworks become central to buyer trust. The country’s Data Privacy Act emphasizes strong privacy protection while still allowing the free flow of information needed for innovation and economic growth. This balance is particularly important for industries such as banking, financial services, insurance, and healthcare, where data governance standards are closely scrutinized by global clients. [80]

Infrastructure cost (power) and reliability. Electricity cost remains a structural constraint. High industrial electricity rates directly affect operations that run around the clock, including contact centers, cloud infrastructure, and data centers. This becomes an even bigger issue as the industry pushes toward higher-value digital workloads that require more compute capacity and stable infrastructure. If power costs remain high relative to competing locations, it can weaken the country’s competitiveness for those types of operations. [81]

Quantifying high-growth segments and revenue opportunity

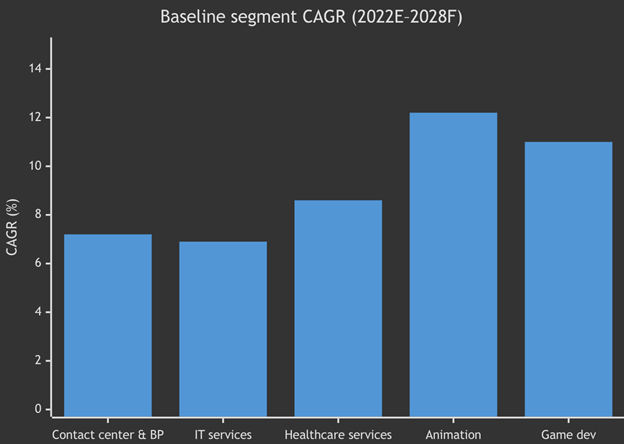

Segment growth rates (roadmap baselines)

The industry roadmap provides baseline growth trajectories for several segments (2022E and 2028F). While some of these categories overlap in practice, the projections still help highlight where the strongest momentum is likely to come from. [82]

Opportunity sizing through 2030 (incremental revenue)

Using 2026 guidance ($42B) as a base and the scenario band above:

- The incremental export revenue opportunity from 2026 to 2030 lands in a clear range. In a constrained scenario, it is roughly $9B. In the upside scenario, it is roughly $17B. The base case sits around $13B of incremental export revenue over that period. [83]

- The highest confidence “where to play” pool is GCC expansion. Starting from about $8B in 2024, even a moderate double-digit growth rate could bring GCC revenue to roughly $14B to $22B by 2030. That is about $6B to $14B of incremental GCC revenue on its own. [2]

- The other scaled bets are verticals where demand is already concentrated, especially BFSI and healthcare. With BFSI already over 25 %of the mix and healthcare around 11 to 15 %, even holding share while total industry revenue rises, produces large absolute gains. The bigger upside comes from moving up the value chain within these verticals. More analytics-heavy work and more compliance-heavy workflows typically increase revenue per FTE and make the work stickier through budget cycles. [84]

Actionable implications by stakeholder

For investors (services and infrastructure)

The strongest risk-adjusted investment thesis sits along the GCC and digital infrastructure axis. GCC expansion is widely identified as a faster growth lane and one that generates higher revenue per employee. At the same time, large capital deployments into data centers, telecom towers, and fiber networks show that investors view the infrastructure layer as essential to the services ecosystem. These two layers reinforce each other. GCC expansion increases demand for reliable infrastructure, and stronger infrastructure makes large-scale delivery operations more feasible. [85]

For service providers

The most durable strategy is to treat AI not as a simple productivity tool but as a redesign of how work gets done. That means shifting more talent into areas such as cybersecurity operations, cloud management, data and analytics work, and domain-specialized services tied to industries like finance and healthcare. Providers that bundle multiple capabilities into transformation deals tend to create more durable client relationships. Expanding delivery into regional hubs can also reduce geographic concentration risk while maintaining service quality and access to talent. [86]

For policymakers

The key challenge is making the Philippines easier for global firms to scale operations responsibly. This involves stabilizing how incentives are implemented and ensuring that national policies align clearly with local government units. It also means supporting credible hybrid and work-from-home frameworks that help the industry maintain access to talent. Continued investment in connectivity infrastructure and addressing high power costs are equally important because both factors directly affect round-the-clock service delivery and the growth of digital infrastructure. [87]

References

[1] BusinessWorld Online. (2023, March 1). IT BPM sector revenues increase by 10% in 2022. https://www.bworldonline.com/top-stories/2023/03/01/507574/it-bpm-sector-revenues-increase-by-10-in-2022/

[2] BusinessWorld Online. (2025, June 11). Philippine IT BPM industry expected to outpace global growth. https://www.bworldonline.com/top-stories/2025/06/11/678403/philippine-it-bpm-industry-expected-to-outpace-global-growth/

[3] IT and Business Process Association of the Philippines (IBPAP). (n.d.). [Industry roadmap report]. https://admin.ibpap.org/storage/hub-resources/1fntWJGQKvZg4CfwP4yfXs0Jr1n85DVR1vYXJvSn.pdf

[4] Reuters. (2024, October 2). Philippine outsourcing to grow 7% this year despite AI threat, industry group says. https://www.reuters.com/technology/artificial-intelligence/philippine-outsourcing-grow-7-this-year-despite-ai-threat-industry-group-says-2024-10-02/

[5] BusinessWorld Online. (2025, September 24). IT BPM industry still bullish on growth. https://www.bworldonline.com/top-stories/2025/09/24/700403/it-bpm-industry-still-bullish-on-growth-2/

[10] Philippine News Agency. (n.d.). [Article 1220220]. https://www.pna.gov.ph/articles/1220220

[17] Gartner. (2026, February 3). Gartner forecasts worldwide IT spending to grow 10.8% in 2026, totaling $6.15 trillion. https://www.gartner.com/en/newsroom/press-releases/2026-02-03-gartner-forecasts-worldwide-it-spending-to-grow-10-point-8-percent-in-2026-totaling-6-point-15-trillion-dollars

[18] International Monetary Fund. (2026, January). World Economic Outlook Update (January 2026) [PDF]. https://www.imf.org/-/media/files/publications/weo/2026/january/english/text.pdf

[44] Department of Information and Communications Technology. (n.d.). [News update 25583]. https://dict.gov.ph/news-and-updates/25583

[51] Knight Frank. (2024, March 26). The offshoring sector in the Philippines enters a new era of growth and transformation. https://www.knightfrank.com/research/article/2024-03-26-the-offshoring-sector-in-the-philippines-enters-a-new-era-of-growth-and-transformation

[59] BusinessWorld Online. (2025, April 30). Philippines’ IT BPM sector to cross $40B in revenues this year. https://www.bworldonline.com/top-stories/2025/04/30/669235/philippines-it-bpm-sector-to-cross-40b-in-revenues-this-year/

[62] Philippine Information Agency. (n.d.). DICT’s connectivity initiatives envision a digitally inclusive nation. https://pia.gov.ph/news/dicts-connectivity-initiatives-envision-a-digitally-inclusive-nation/

[63] BusinessWorld Online. (2025, December 3). Data center operators form alliance to support industry growth. https://www.bworldonline.com/corporate/2025/12/03/716051/data-center-operators-form-alliance-to-support-industry-growth/

[64] World Trade Organization. (n.d.). Philippines case study [PDF]. https://www.wto.org/english/tratop_e/ts4d_e/case_studies_e/philippines.pdf

[65] BloombergNEF. (n.d.). Philippines. Climatescope. https://www.global-climatescope.org/markets/philippines

[67] Department of Finance. (n.d.). IT BPM firms may choose to adopt WFH arrangements but must comply with conditions in operating in ecozones to continue enjoying incentives. https://www.dof.gov.ph/it-bpm-firms-may-choose-to-adopt-wfh-arrangements-but-must-comply-with-conditions-in-operating-in-ecozones-to-continue-enjoying-incentives/

[68] Department of Finance. (n.d.). Recto: CREATE MORE law is a win win for both businesses and the Filipino people. https://www.dof.gov.ph/recto-create-more-law-is-a-win-win-for-both-businesses-and-the-filipino-people/

[69] Philippine News Agency. (n.d.). [Article 1244560]. https://www.pna.gov.ph/articles/1244560

[72] Philippines’ PLDT in talks to sell up to 49% of data centre business to Japan’s NTT. (2024, May 7). Reuters. https://www.reuters.com/markets/deals/philippines-pldt-talks-sell-up-49-data-centre-business-japans-ntt-2024-05-07/

[74] KKR to invest $400 million in Philippine telecoms tower business. (2024, March 13). Reuters. https://www.reuters.com/business/media-telecom/kkr-invest-400-mln-philippine-telecoms-tower-business-2024-03-13/

[76] Alibaba Cloud announces new data centres in Malaysia, Philippines. (2025, July 2). Reuters. https://www.reuters.com/world/asia-pacific/alibaba-cloud-announces-new-data-centres-malaysia-philippines-2025-07-02/

[80] National Privacy Commission. (n.d.). Data Privacy Act of 2012 (Republic Act No. 10173). https://privacy.gov.ph/data-privacy-act/

[87] PricewaterhouseCoopers (PwC) Philippines. (2024). Tax Alert No. 44: CREATE MORE [PDF]. https://www.pwc.com/ph/en/tax/tax-alerts/2024/pwcph-tax-alert-44-create-more.pdf