Executive Summary

Outsourcing in 2026 is still about delivering results when conditions are tight.

Companies need stable operations and consistent customer experience at the same time budgets are under pressure, risk is higher, and key skills are harder to hire and keep. What changed is not that cost no longer matters. It still does, but that “good performance” is now judged by more than price.

Buyers are increasingly willing to pay for providers that can get capabilities live faster, use AI in day-to-day delivery without creating new exposure, and keep services running reliably across multiple locations and rules.

A defining feature of 2026 is that enterprise technology demand is growing, but spending is being directed more selectively.

Investment is accelerating where it supports cloud platforms, data, security, and AI infrastructure. Meanwhile, traditional managed services growth is more constrained and deal activity is concentrating into fewer, more strategic transactions. That split matters because it mirrors the buyer mindset: many organizations are outsourcing not just to run work cheaper, but to modernize work while it runs—and they are demanding tighter governance and clearer proof of results in return.

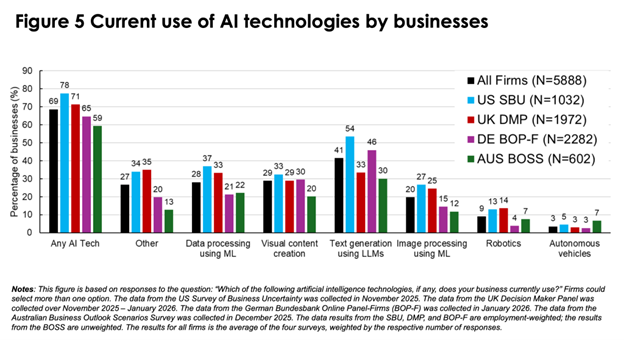

In 2026, the “new normal” is collision of four forces. First, AI is now assumed in RFPs and delivery models, but measurable enterprise-wide return is still uneven. Deloitte reports that 83% of surveyed executives are leveraging AI as part of their outsourced services, while also highlighting that governance and contracting challenges have limited realized benefits to date.

The tension is reinforced by a 2026 NBER working paper based on surveys of roughly 6,000 senior executives across four advanced economies, where a large share report active AI use but 89% estimate no productivity impact over the last three years, even as expectations rise for the next three.

Second, regulation has moved from background context to delivery constraint. The EU AI Act’s implementation timeline now sets concrete readiness expectations: prohibited practices apply from February 2025, general-purpose AI obligations apply from August 2025, and full applicability arrives in August 2026 with certain high-risk transitions extending to 2027. Parallel cybersecurity requirements, such as NIS2, with a transposition deadline in October 2024, raise the baseline for third-party and supply-chain accountability.

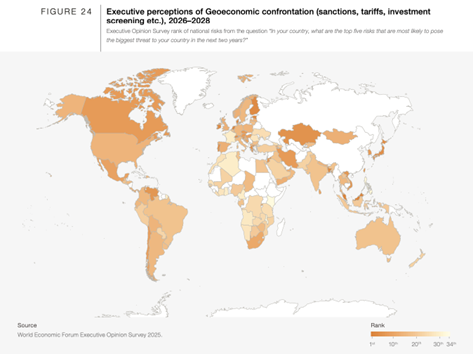

Third, geopolitical risk has reshaped location strategy from a cost exercise into resilience design. The World Economic Forum’s Global Risks Report 2026 highlights “geoeconomic confrontation” as the top risk most likely to trigger a global crisis in 2026.

Fourth, the buyer-provider relationship is increasingly “managed services as product,” where outcomes, subscription constructs, and embedded transformation matter more than “FTEs under supervision.” In the KPMG managed services outlook, speed to market emerges as a top goal and buyers report managed services exceeding expectations in that area.

These conditions have pushed five clear shifts in buyer behavior. Buyers remain cost-sensitive, but they are increasingly judging cost in terms of total cost of ownership and cost-to-outcome, not hourly rates alone. Speed to capability has become a primary requirement where buyers want providers that can bring ready teams, proven playbooks, and faster deployment. They are asking for AI readiness with guardrails, meaning clarity on what tools are used, what data is touched, who oversees it, and how it is logged and audited. They are prioritizing operational resilience, using multi-location delivery and continuity planning as core deal requirements. Finally, they are also asking for outcome-based engagements: SLAs are still needed, but buyers increasingly want KPIs linked to quality, customer results, and, in some cases, financial impact.

For buyers, success in 2026 comes from treating outsourcing as portfolio design, not vendor selection. The best-performing organizations strengthen internal governance, clarify who owns outcomes and measurement, and treat AI governance as part of service management rather than a separate policy exercise. They evaluate providers on delivery maturity and risk posture, not only price and brand. They apply a dual lens assessing whether the provider runs the service reliably today, and can it improve it safely while it runs.

Over the next 12–24 months, the market is likely to keep moving toward outcome-based, AI-enabled managed services, but at uneven speed. Some organizations will scale governed AI in production and see measurable gains; others will accumulate pilots and contracts without hard impact. The difference will largely come down to whether governance, data discipline, and change management are treated as core workstreams rather than optional support.

Market Overview & Key Statistics

Where We Are Now

Outsourcing remains relevant in 2026 because it sits at the intersection of three pressures that companies cannot easily solve through internal hiring alone. These are rising technology investment, ongoing cost pressure, and higher risk from regulation, cyber threats, and geopolitics. Outsourcing is still one of the few levers that can address all three, but only if it is structured with modern delivery methods and tighter governance.

The market continues to show momentum, but the mix is changing. ISG’s index signals that growth is stronger in cloud and “as-a-service” consumption models, while more traditional managed services growth looks more selective and concentrated in fewer strategic deals. In practical terms, buyers are spending aggressively where services are scalable and tied to platforms, while being more cautious about labor-heavy discretionary scope. This is why 2026 feels polarized because spending is up, but scrutiny is up as well.

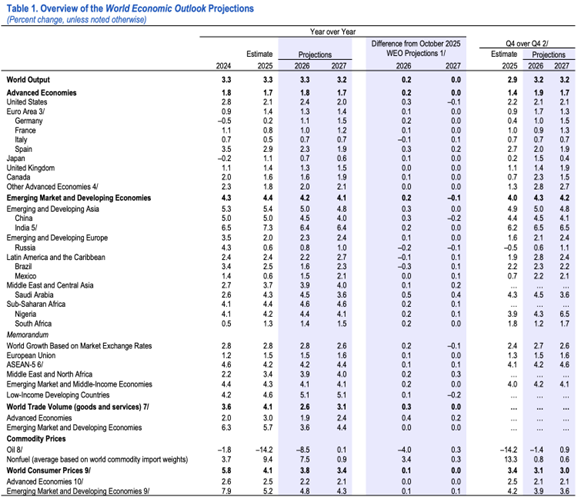

Cost pressure is also more complex than headline inflation alone. The IMF projects global headline inflation declining to 3.3% in 2026 and 3.2% in 2027, alongside global growth around 3.3% in 2026, which supports a “steady but divergent” macro frame rather than a uniformly easy cost environment.

Even where inflation has eased, buyers still feel cost pressure through wages, churn, training time, and the growing baseline cost of compliance. For outsourcing, this means “delivered cost” varies more by location and industry, and TCO comparisons have become more important than simple rate comparisons. Buyers are asking not only “what does this cost?” but “how stable is the cost, how predictable is delivery, and what risk am I taking on?”

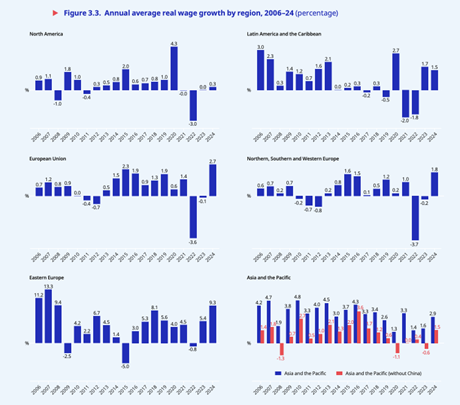

At the same time, wage recovery is uneven and regionally heterogeneous. The ILO’s Global Wage Report indicates global real wage growth returned to positive in 2023 and early 2024, but the report emphasizes continued variation by country and region, which maps directly to uneven delivered cost across major sourcing hubs.

AI acceleration is a major driver of demand, but it affects outsourcing in two distinct ways. Upstream, it increases investment in infrastructure, cloud platforms, security, and data foundations.

Downstream, it raises expectations that providers can run operations with AI assistance while still meeting quality, privacy, and audit requirements.

The gap between AI adoption and measured enterprise impact is one reason buyers are outsourcing not just for tools, but for capability plus operating model change.

Geopolitical and regulatory influences increasingly shape how services are designed and where they run. Location strategy has shifted from “cheapest footprint” to “resilient footprint,” with more emphasis on multi-location coverage, tested continuity, and reduced concentration risk. Regulation is also turning into a delivery constraint: buyers want evidence of compliance readiness, clear data handling, and strong third-party controls, especially in regulated sectors.

Geopolitical and regulatory influences increasingly shape how services are designed and where they run. The WEF’s framing of geoeconomic confrontation as a leading 2026 crisis-trigger risk puts more emphasis on multi-location coverage, tested continuity, and reduced concentration risk. Regulation through the EU AI Act and US state privacy requirements further tighten delivery requirements.

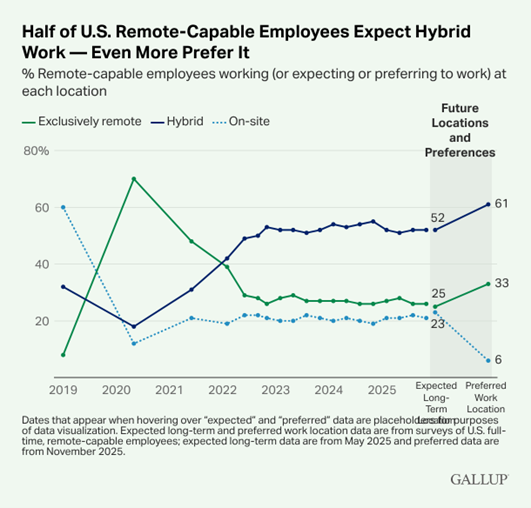

Finally, hybrid and remote delivery are now normalized, which subtly changes the operating context for outsourcing. Gallup’s indicator shows that among remote-capable employees, hybrid is the preferred arrangement for a majority, with about one-third preferring fully remote and fewer than one in ten preferring fully on-site.

For outsourcing, this normalization reduces collaboration friction between internal and external teams and increases expectations for secure, auditable remote delivery—identity controls, data governance, and operational transparency become baseline design requirements rather than special accommodations.

What Buyers Want in 2026

Cost Is Still Important, but It Is Not the Only Driver

Cost remains a core reason to outsource, but buyers are changing how they define savings. Instead of focusing mainly on labor arbitrage, many buyers are pursuing lower cost-to-outcome through process redesign, automation, and stronger operating controls.

In practice, this shifts the conversation from “what is the hourly rate?” to “what is the cost per resolved case, cost per compliant onboarding, or cost per stable workload managed?”

Total cost of ownership has become a more serious decision tool. Buyers increasingly include the cost of governance, compliance work, training time, rework, and change management in their comparisons.

This is also why some buyers prefer predictable operating expense models. such as subscription-style managed services, over internal build, particularly when internal hiring is slow and execution risk is high in specialized domains.

What this means for providers

Providers that win in 2026 look less like labor aggregators and more like operators of a governed delivery system. They will be expected to:

- Demonstrate AI-augmented delivery

- Offer credible compliance-by-design

- Bring commercial flexibility

- Prove depth in scarce talent domains

What this means for buyers

Buyers who win in 2026 treat outsourcing as portfolio design, not vendor selection. That means:

- Building stronger internal governance

- Evaluating providers on delivery system maturity and compliance posture

- Using a dual lens: “Can this provider run today’s process reliably?” and “Can this provider modernize the process safely while it runs?”

Looking ahead

Over the next 12–24 months, outsourcing will continue to shift toward outcome-based, AI-enabled managed services, but adoption will be uneven. Macro conditions are improving in some dimensions (easing headline inflation) while risk remains structurally elevated (geoeconomic confrontation, cyber insecurity, regulatory deadlines).

Buyers and providers that treat governance, data, and change management as first-class workstreams will convert AI and sourcing into a durable advantage; others will accumulate pilots, contracts, and compliance exposure without business impact.

What Buyers Want in 2026

Speed to Capability

Speed is now crucial for gaining a competitive edge. Companies focus on quickly deploying new capabilities instead of just improving existing processes. Buyers are outsourcing to find skilled teams and proven strategies that help them achieve results faster.

According to the KPMG managed services outlook, getting new products and services to market quickly is the top priority for buyers, and they report that this outsourcing model is meeting their expectations.

In practice, this “speed” is less about how fast vendors work; it’s also about avoiding the slow internal processes like hiring and setting up systems.

Buyers want service providers that can seamlessly integrate AI into their operations. This means using AI within workflows, determining where human oversight is needed, setting up monitoring systems, and ensuring there’s clear evidence of control.

Risk Mitigation and Operational Resilience

Resilience is becoming an important factor in business deals. Due to geopolitical uncertainty, there’s a higher risk of disruptions in locations, trade, data restrictions, and sudden regulatory changes. The World Economic Forum highlights the need for multi-location strategies and proven continuity plans in sourcing.

Cyber risks add to this concern, as relying on a single provider can lead to significant operational disruptions. Regulatory requirements are also making third-party risk management more stringent, especially in the EU with the NIS2 directive, which strengthens governance and supply chain responsibilities.

In 2026, resilience isn’t just about having an alternative site. It involves having tested plans for switching operations, clear decision-making processes during incidents, defined data access controls, and procedures that comply with regulations even during disruptions.

Buyers are increasingly willing to accept short-term cost increases, like maintaining duplicate capabilities and implementing stronger controls, because the potential costs of outages, data breaches, or regulatory fines are seen as more significant.

Outcome-focused engagement

Focusing on outcomes is a major shift that aligns with the reality of AI. If AI is widely used but productivity gains are inconsistent, buyers will push providers to commit to measurable performance indicators (KPIs) and share risks in achieving them. Deloitte’s research shows that while AI-powered outsourcing is common, challenges in governance and contracts have limited benefits.

This is why buyers are increasingly demanding measurement, accountability, and alignment in 2026.

Outcome-based engagement changes the focus from hours worked to performance results. This includes faster cycle times, improved quality, less rework, better compliance, enhanced customer outcomes, and sometimes even linking to revenue impacts. While service level agreements (SLAs) remain important, they are now seen as basic requirements, with outcomes becoming the key differentiator.

What this means for vendors

In 2026, successful providers will operate as governed delivery systems rather than just labor aggregators. Their strength will come from consistent execution, built-in modernization, audit-ready controls, and commercial alignment that can withstand scrutiny.

Delivery models are shifting toward “as-a-service operations,” reflecting the trend from traditional managed services to more flexible offerings. Winning providers will standardize their services with measurable performance and provide clear modernization plans that integrate running and transforming operations without forcing clients into disruptive changes.

Expectations for AI in the workforce are now practical. Buyers want to know how AI is used, what controls are in place, how bias and explainability are managed, and how clients can audit these processes. Deloitte’s survey shows that while AI is common in outsourced services, there’s a governance and contracting maturity gap that limits its impact. Providers that can effectively integrate AI into workflows and measurement will stand out, especially since many firms report no productivity gains despite adopting AI.

Investing in compliance and governance has become essential for growth, not just a business cost. With regulations like the EU AI Act and NIS2 cybersecurity requirements, buyers will demand evidence of compliance readiness, including traceability and transparency. Providers that view governance as part of their delivery infrastructure will be more successful in regulated markets.

Flexibility in commercial models is important but must be supported by strong operational frameworks. Subscription services, modular bundles, and risk-sharing mechanisms need robust measurement and attribution systems. Providers that can design and maintain these frameworks will outperform those that only offer creative pricing.

Talent depth is becoming more valuable than simply having a large workforce. While buyers still care about coverage and continuity, they are willing to pay more for expertise in cloud/AI infrastructure, security, analytics, and product operations, as well as for stability in critical roles during turnover.

What this means for buyers

Buyers in 2026 need to improve their sourcing operations. The main gaps often lie not in procurement but in governance, measurement, and cross-functional ownership, especially for AI-enabled services. Deloitte’s survey shows that many executives feel their vendor management functions are not fully developed, and traditional vendor management offices (VMOs) often lack a comprehensive workforce strategy. This gap becomes evident when buyers try to implement outcome-based models without clear ownership of key performance indicators (KPIs) or when introducing AI without established policies for tool use, data access, monitoring, and auditing.

As a result, vendor evaluation criteria are broadening beyond just cost and references. Buyers are now looking at the maturity of a provider’s delivery system, AI controls and transparency, resilience design, and commercial alignment. A provider’s reputation matters less than their ability to deliver measurable outcomes that can withstand scrutiny from boards and regulators.

Focusing solely on price can lead to significant risks in 2026. Low rates may come with hidden total costs of ownership (TCO) due to governance issues, rework, delays, and change fatigue. Compliance risks increase as privacy and AI regulations require demonstrable controls. The likelihood of disappointment with AI also rises if it is adopted without proper workflow redesign and measurement, which aligns with the gap between AI adoption and actual productivity gains reported by executives.

Buyers are now asking. They want to know how productivity and quality will be measured and audited, which AI tools will be used, what data they will access, what continuity scenarios have been tested, and what decision points clients have. They also want clarity on how providers commit to outcomes versus service level agreements (SLAs), including what happens if outcomes are not met. These questions are crucial for ensuring controlled modernization and managing risks effectively in 2026.

Key metrics and benchmarks to watch

Outsourcing maturity requires metrics that link operational performance to business value, automation, and compliance.

While adhering to service level agreements (SLAs) is still important for reliability, it’s no longer enough for governance or discussions about value.

Key Metrics for Buyers and Providers

Mature buyers and providers are increasingly tracking automation metrics to measure efficiency, such as the percentage of transactions handled by automation or AI and the rates of straight-through processing. They also monitor quality and rework metrics, including defect escape rates, re-open rates, audit findings, and complaint causes. This is important because weak controls can lead to a trade-off between speed and quality when using AI and automation.

Focus on Outcome Metrics

Outcome metrics are becoming more critical, including improvements in cycle times, reductions in service costs, onboarding times, customer satisfaction factors, and fewer regulatory issues. Compliance metrics are now essential governance tools, such as completion of access reviews, incident response performance, AI usage logs, and third-party risk controls.

In 2026, enterprises want solid evidence. These metrics serve as proof that supports those outcome-based contracts.

Strategic outlook: 12 to 24-month signals

The goal in this section is to identify signals with credible evidence that may shape decisions through 2026–2027.

1. AI-Driven Workforce Redesign

AI infrastructure spending is increasing, but the productivity impacts at the firm level are inconsistent. This often leads to a shift from just adopting tools to redesigning workflows, improving governance, training, and changing operating models. Expect to see deals that include specific “AI operating model” components, such as policies, monitoring, traceability, and role definitions, rather than just access to AI tools.

2. Increased Outcome-Based Contracting

As buyers demand proof of results and providers market managed services like subscriptions, hybrid commercial models combining base fees with measurable outcome incentives will likely grow. This is especially true where reliable attribution frameworks exist and demand variability can be managed.

3. Growth of Specialized Outsourcing

Spending is increasingly directed toward specialized areas like cloud, AI infrastructure, cybersecurity, and engineering. This trend reflects the ongoing investment cycle in AI and cloud technologies and aligns with buyers’ preferences for quick access to capabilities.

4. Pressure on Mid-Tier Providers

As governance, compliance, and AI capabilities become essential for strategic deals, mid-tier providers that cannot invest in these areas may struggle to compete against larger platforms and specialized firms. This doesn’t mean mid-tier providers will decline, but differentiation will become clearer, and underinvestment will be more noticeable.

5. Rise of Hybrid BPO and GCC Strategies

Enterprises are blending models, using internal centers for specialized capabilities while relying on providers for standardized operations and transformation. This will lead to more complex management of portfolios and necessitate stronger governance to ensure integration and avoid fragmentation.

These signals can combine in different ways:

Optimistic Scenario: AI-managed services evolve from pilot programs to full-scale workflows, with buyers and providers aligning on measurable outcomes, supported by strong IT spending growth.

Cautious Scenario: Adoption continues, but realizing value is slow due to governance issues and measurement challenges, consistent with gaps highlighted in executive surveys.

Disruptive Scenario: Economic shocks or regulatory changes prompt rapid shifts in locations and increase compliance costs, leading to swift consolidation and restructuring of global delivery systems.

Methodology and References

This report summarizes research and market indicators from 2024 to February 2026, focusing on recent market and regulatory developments.

Market Trends: Insights are based on ISG Index reports for Q4 2025 and the full year of 2025.

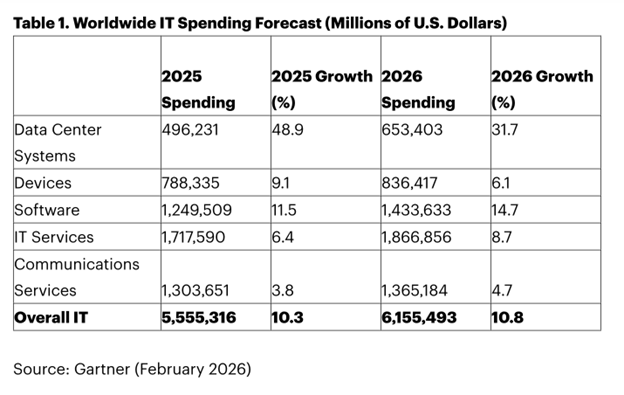

Technology Spending: Information comes from Gartner’s 2026 IT spending forecast.

Macroeconomic Context: Data is sourced from the IMF’s January 2026 World Economic Outlook Update.

Labor and Wages: The ILO Global Wage Report 2024–25 provides relevant insights.

Buyer Behavior: Findings are drawn from Deloitte’s Global Outsourcing Survey 2024 and KPMG’s managed services outlook.

Geopolitical Risks: The World Economic Forum’s Global Risks Report 2026 offers context.

Regulatory Framework: Information on the EU AI Act and NIS2 is referenced from official EU policy pages.

AI Adoption: A 2026 NBER working paper discusses AI productivity based on executive surveys in advanced economies.

Privacy Regulations: U.S. state privacy trends and India’s DPDP rules are covered through IAPP reporting and Indian government notifications.